The Multi-Step Income Statement is a financial reporting format where a company’s revenue, costs, and expenses are classified into separate categories before arriving at net income (the “bottom line”).

Table of Contents

The multi-step income statement is a method of presenting the financial results of a company by segmenting the revenue, costs, and expenses into distinct sections.

The components of the multi-step income statement comprise three equations that calculate a profit metric that each measures a unique attribute of the underlying company’s financial performance.

By separating the income statement, or profit and loss statement (P&L), into multiple sections, the presentation of the financial statement offers more in-depth information on the company’s performance to facilitate a more detailed analysis to better comprehend its business model and operating drivers.

In particular, there are three equations that underpin the multi-step income statement:

Starting off, the gross profit is equal to the revenue generated by a company in a pre-defined period minus its cost of goods sold (COGS), which are the direct costs incurred as part of its core business operations.

Gross Profit = Revenue – Cost of Goods Sold (COGS)The COGS line item includes the direct costs of producing the goods or services sold by a company to produce revenue, such as the following:

From the gross profit line item, the next profit measure is the operating profit, or “EBIT,” an abbreviation for “Earnings Before Interest and Taxes.”

Operating Profit (EBIT) = Gross Profit – Operating ExpensesLike COGS, operating expenses are an integral part of the core operating activities of a company. However, operating expenses are not directly related to the revenue model of the company.

Some of the more common examples of operating expenses are as follows.

The third and final component of the multi-step income statement is net income (the “bottom line”), which represents the net profitability of a company per accrual accounting standards.

The net income metric is inclusive of all costs – operating and non-operating costs – in contrast to the operating profit metric, which only accounts for operating costs (i.e. COGS and Opex).

Therefore, the net income factors in non-operating items such as interest expense, other non-operating costs such as non-recurring losses from inventory write-downs, and income taxes paid to the government.

The net income equation is as follows.

Net Income = Operating Profit – Non-Operating CostsContrary to operating costs, non-operating costs are not part of the core, recurring operating activities of a company.

For instance, interest expense is a non-operating cost since the item pertains to the financing activities of a company rather than any of its specific operating activities.

The difference between the single-step and multiple-step income statement is as follows.

Fundamentally, the basic premise of either presentation format is conceptually the same, granted the outcome of either method is to arrive at net income.

Yet, from a practical perspective, the insights that can be obtained from the multi-step income statement are ultimately far more insightful to understand and analyze the financial performance of a company.

Under the single-step income statement, the core equation is as follows.

Net Income = Revenue – (Cost of Goods Sold + Operating Expenses + Non-Operating Expenses)While the single-step format might be sufficient for certain small companies, such as a local family-owned business, the decision to raise capital from investors or to borrow debt capital from lenders causes the reporting style to become impractical.

In short, the introduction of stakeholders for the first time is typically the catalyst for private companies to transition from the single-step to multiple-step income statement.

For public companies, there are strict reporting guidelines established where a single-step format is not even an option.

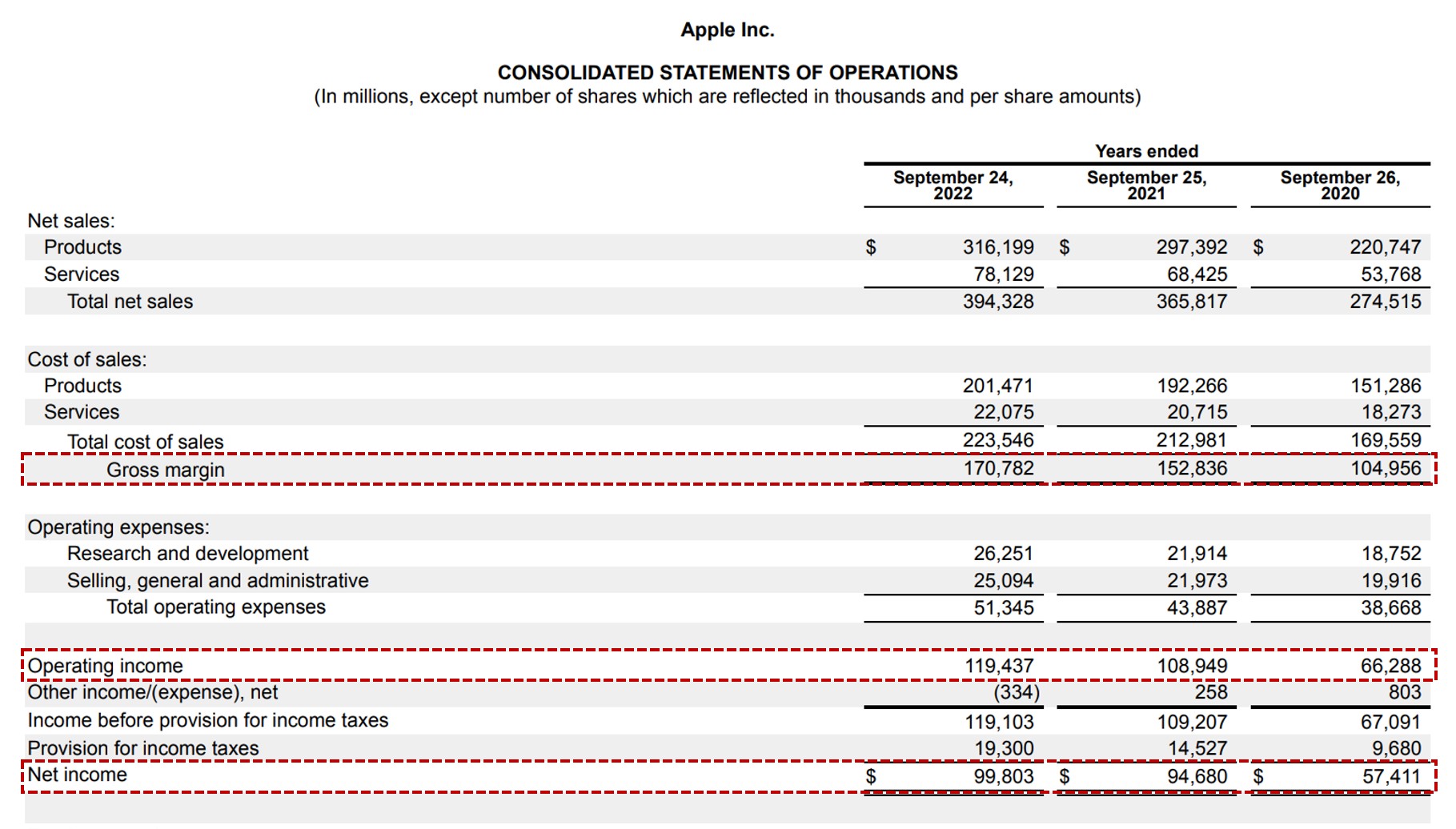

Each of the three profit metrics—gross profit, operating income, and net income—are highlighted on the income statement of Apple (AAPL).

Apple Income Statement (Source: AAPL FY-2022 10-K)

We’ll now move to a modeling exercise, which you can access by filling out the form below.

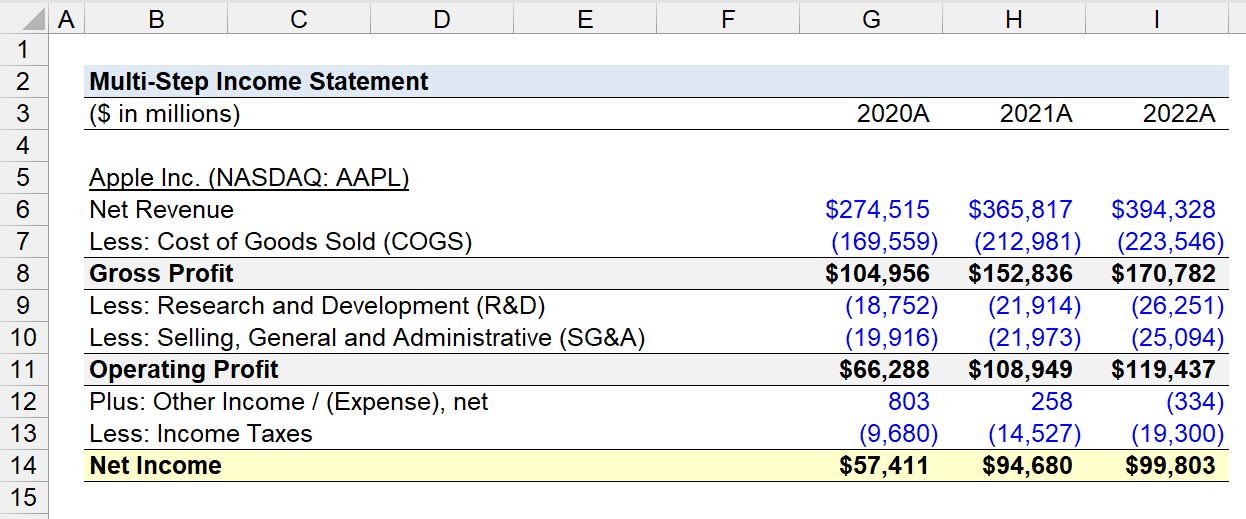

Suppose we’re tasked with preparing a multi-step income statement for Apple (NASDAQ: AAPL) for fiscal years ending 2020 to 2022.

Based on the latest 10-K filing of Apple (AAPL), we’ll input the historical income statement data into our spreadsheet using the proper formatting convention, in which hard-coded figures are entered in blue font while calculations are left in black font.

The first step is to compute the gross profit of Apple in each period using the following set of equations:

Given the gross profit of Apple for each period, the next step is to subtract operating expenses to determine the company’s operating profit in each fiscal year.

In the final step, the remaining equation solves for the net income of Apple in our trailing three-year period.

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.